18-06-2019

Travel insurance, does it really worth it?

Sophie

This question is recurrent in the world of travel. People often think that the RAMQ (Régie de l’Assurance Maladie du Québec) covers everything, but they are mistaken. Same story compared to the insurance offered by credit cards or group insurance at work; most offer only minimal coverages. That is why it is important to always find out what is covered or not, for example, does your insurance cover repatriation in the event of a natural disaster, land or air transport in the event of an injury requiring emergency transportation to hospital, damaged or lost luggage, missed connections due to delayed flights …? So many things that we take for granted but most of time are not covered by these plans. First, it should be noted that the services covered by the RAMQ during a stay outside Quebec are not the same as those covered within the province. And as most of the people we spoke to honestly believed that the cover of the sun card is sufficient to cover all medical expenses outside Quebec, we thought we should copy the text found on the Quebec government’s website in this regard:

When travelling or when outside Québec temporarily, persons holding a valid Health Insurance Card can receive healthcare services covered by the Québec Health Insurance Plan. However, in most cases, RAMQ reimburses only part of the cost.

In order for these services to be covered, persons spending time outside Québec must fulfill certain conditions regarding the duration of their trip or temporary stay. Information about remaining eligible for the Health Insurance Plan is available in the section on eligibility during a stay outside Québec.

And that’s not all, they add this box to highlight the fact that private insurance is a must when you leave Quebec.

Private insurance: To avoid unfortunate consequences

When spending time outside Québec, it’s a good idea to take out private insurance before leaving. Generally speaking, RAMQ does not reimburse the full cost of healthcare services received outside Québec and certain services are not covered by the Health Insurance Plan at all. If you receive healthcare outside Québec but don’t have private insurance, you are responsible for the portion of the cost not reimbursed by us. Information about private insurance is available from the OmbudService for Life & Health Insurance (OLHI).

And so that you understand the full scope of the disadvantages that can arise when your coverage is not sufficient, we have selected 2 examples, cited on the website of the RAMQ, which proves how we can find ourselves in a precarious situation after a simple injury as after a more serious incident … After all, when an accident or inconvenience occurs, the last thing we want to face is the financial worries.

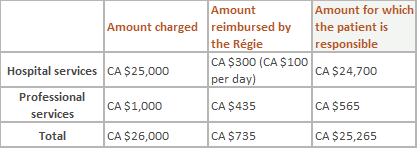

Example of the amount reimbursed by the Régie where an insured person is hospitalized in intensive care for 3 days in Florida for a heart attack

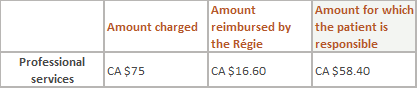

Example of the amount reimbursed by the Régie where an insured person sees a general practitioner in Florida

And to finish with the official information of the RAMQ site, here is a sample of what is NOT COVERED:

Services not covered

Some services received outside Québec are not covered by the Health Insurance Plan. If you don’t take out private insurance for these services before leaving Québec, you must pay their full cost yourself. Here are a few examples:

- any medical services not covered in Québec

- services rendered by a health professional other than a doctor, a dentist or an optometrist

- the cost of a private or semi-private hospital room

- emergency transportation, by ground or air

- the cost of bringing a person back to Québec

- drugs purchased outside Québec, even if prescribed by a physician (before leaving Québec, persons who regularly take prescription drugs can ask their pharmacist whether they may obtain the drugs they will need during their absence)

So, after this informative reading, you are now aware of the importance of checking whether you are insured for travel with your personal insurance, your credit card or even through the group insurance plan of your work, but most of all, you are to verify about what is covered or not. And this logic is essential both for leisure travels and/or business travels. There are also some plans designed for companies with a large volume of business travelers, both within Canada and internationally. When you have to leave the country for business, you imagine every time that everything will go well because it is only a business trip … But what to do when it is not the case? You do not want to be forced to pay expensive medical expenses in another country. And no one wants to break their head for lost luggage or lose money because of a canceled trip, which often happens in corporate travel. That is why travel insurance is more than useful, whether your trips are for pleasure, for business, or both. At Groupe Voyages VP, we are aware that all these different plans are confusing and that it is easy to get lost in all that is offer, so we chose Manulife Insurance Company for the quality, simplicity and diversity of his products. For example, for leisure travel, the Premium Protection Plan is the plan to consider. Unique in its kind, it offers increased coverage and reduced restrictions and is specifically designed for Canadian residents. It allows you to cancel your trip for any reason, even 24 hours before departure. Weather is not nice? You can cancel … Your dog gets sick? You can cancel … You separated from the person who was to accompany you? You can cancel … This protection is simply the most flexible of the market. Since Premium Protection Plan is only available through travel agencies and / or agents, we invite you to contact one of our travel professionals to learn more about this simple and beneficial plan.

At the corporate level, our clients focus on Manulife Global Travel Insurance, which provides coverage for all your trips for one year with an annual plan. This scheme offers:

One-year coverage: You are covered for unlimited travel for 365 days from the effective date, which, let’s face it, is perfect for business trips.

Savings: Often, it’s cheaper than subscribing to two unique travel plans; while traveling for business and / or pleasure, you will be a winner.

A non-negligible advantage: You do not have to worry about your travel insurance for a whole year.

Flexibility: For medical coverage only, choose the annual Emergency Medical Care Plan; but to cover expenses for medical emergencies, loss of luggage, trip cancellation and more, choose the annual full package. You can also choose the maximum duration (8, 16 or 30 days) for each trip – the Emergency Medical Plan also provides you with an annual option for 4, 10, 18, 30 or 60 days.

Conclusion: Never travel without insurance if you come out of the province of Quebec and especially, contact a professional Travel Group VP who will be happy to learn about the travel insurance plan that best suits the type of traveler that you are.

Testimony:

A frightening cardiac event is not so selfie-worthy, but Manulife Travel Insurance made it a little easier to handle for Niall.

Niall is a pretty fit guy. He’s an avid cyclist who had never had any major health issues. In some ways he’s the kind of person you might think would feel safe travelling without insurance. But the Thornhill, ON native says, “I’m a firm believer that things happen and I never wanted to take the financial risk or gamble. That’s why insurance is there. And for the minimal cost of protection, it was peace of mind.”

That philosophy paid off for Niall during a recent trip to San Francisco. He and his wife were simply walking around the city, enjoying the sights, when he started to feel some numbness in his arms and chest. He thought it was weird, but got through the night without issue. The next day, while touring the city, the symptoms reappeared. He would stop and the symptoms would go away, but every time he started walking again, they’d come back.

Finally, he decided to get checked out. But before he did, he called Manulife to let them know. They gave him a case ID number and told him to go to the hospital and keep them up to date. It’s a good thing he went, because he was diagnosed with a cardiac event caused by three blocked arteries and underwent a procedure to rectify the problem.

All told, his entire $64,690.06 medical bill was paid by Manulife. “You hear about these issues people have with insurance companies,” he said, “But never, ever did we ever have any sort of ‘don’t do this or don’t do that.’ They were just very cooperative and very accommodating during the whole process.”